Covariance and correlation both measure how two random variables behave in conjunction with one another, but correlation is a normalized measure scaled to the interval [-1, 1], while covariance is unbounded. Positive covariance or correlation implies that as the value of one random variable increases, the values of the other also increase. Negative implies that as the value of one random variable increases, those of the other decrease, or vice versa.

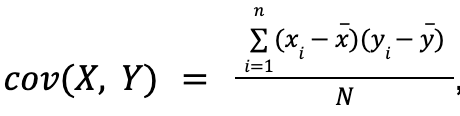

For two random variables X and Y, Covariance is found by:

where ![]() and

and ![]() correspond to the sample means of X and Y, respectively.

correspond to the sample means of X and Y, respectively.

Correlation is then found by:

![]()

where ![]() and

and ![]() refer to the standard deviations of X and Y, respectively.

refer to the standard deviations of X and Y, respectively.